Amiya Kumar

Amiya Kumar

Japan’s Economic Crisis: From Post-War Miracle to Demographic Squeeze (1945–2026)

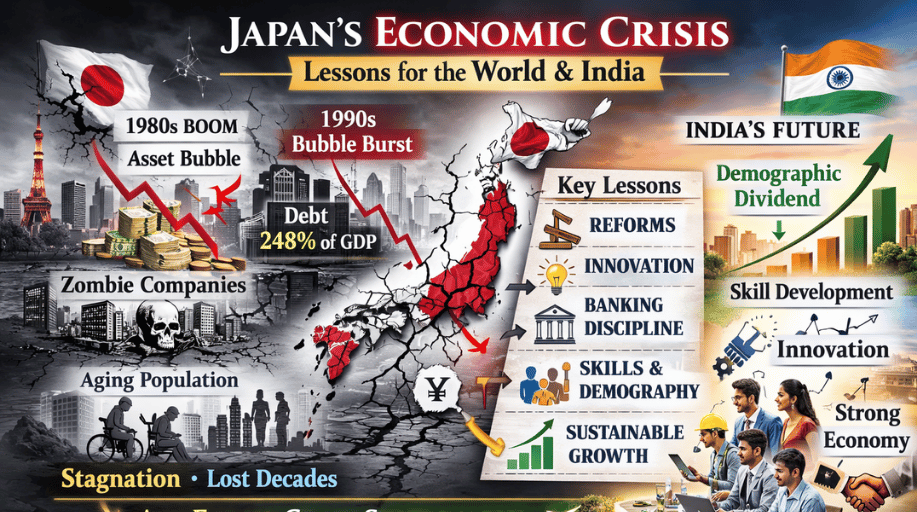

When students discuss Japan’s crisis, they often describe it as an economic collapse. That framing is inaccurate. Japan is not collapsing in the way emerging economies collapse. Japan is experiencing a prolonged structural compression driven by three interlinked forces: an asset-bubble hangover, policy-induced stagnation, and an unprecedented demographic inversion.

To understand the present, we must begin with the height from which Japan fell.

The Post-War Miracle: How Japan Became an Economic Superpower

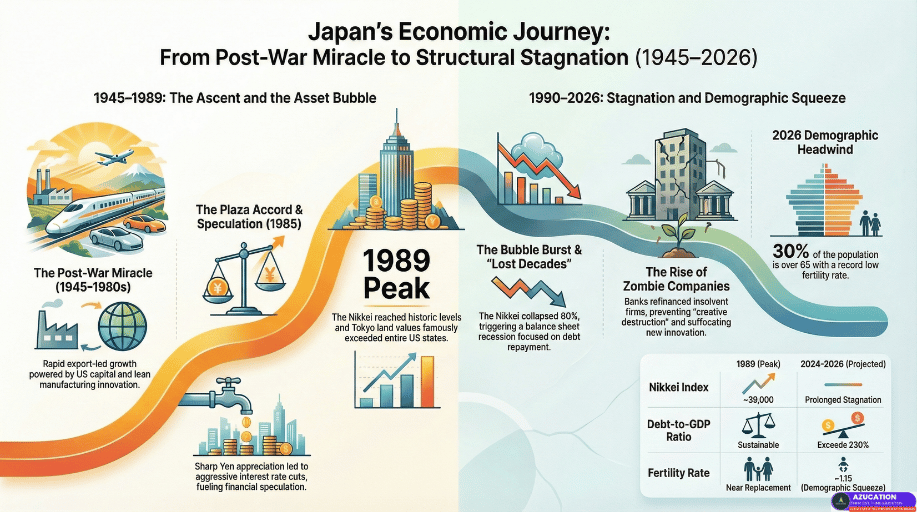

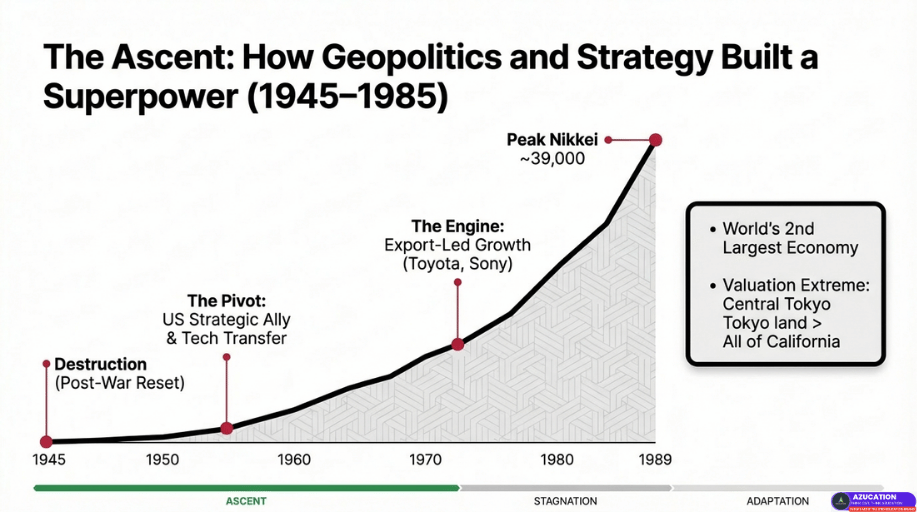

In 1945, Japan was physically and economically destroyed. Two atomic bombs, mass bombing of major cities, industrial collapse, food shortages — the country’s productive capacity was shattered.

However, geopolitics reshaped its destiny.

During the early Cold War, the United States feared communist expansion across Asia. Instead of punishing Japan economically, the US rebuilt it.

American capital entered Japanese industry. Technology blueprints were shared. Japan adopted an export-led growth model. Firms like Toyota perfected lean manufacturing. Sony innovated in electronics. Toshiba became dominant in memory chips.

By the late 1980s, Japan was the world’s second-largest economy. The Nikkei index surged from around 6,000 in the early 1980s to nearly 39,000 by 1989. Real estate prices soared. Japan appeared unstoppable.

That confidence created fragility.

The Plaza Accord: Currency Shock and the Seed of Instability

In 1985, the United States faced a growing trade deficit. The Plaza Accord was signed to coordinate currency adjustments.

The yen appreciated sharply — from roughly ¥240 per dollar to near ¥120.

To prevent recession, the Bank of Japan slashed interest rates aggressively.

The mistake was not cheap credit. The mistake was its misallocation.

Instead of investing in productivity, corporations and individuals diverted funds into financial speculation. Stock prices surged. Real estate detached from reality. The economy entered bubble territory.

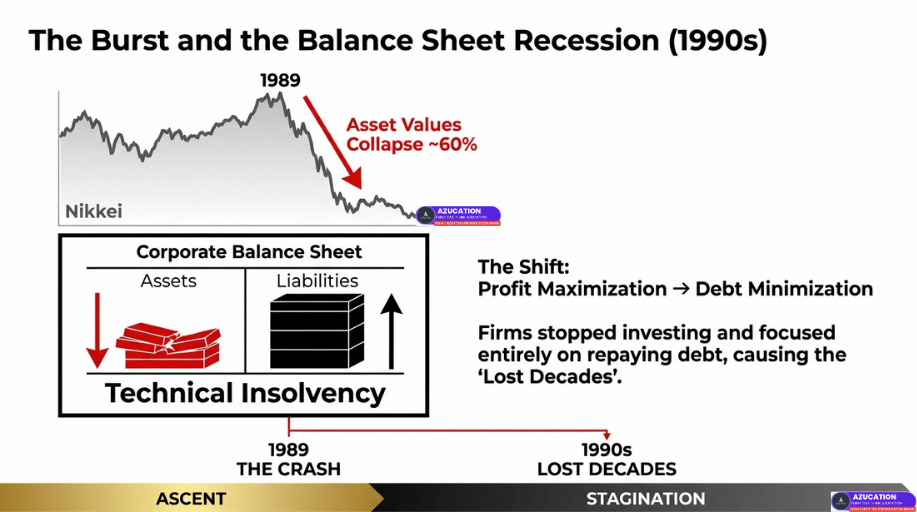

The Bubble Burst and the “Balance Sheet Recession”

In 1989, the Bank of Japan raised interest rates. The bubble burst.

The Nikkei collapsed nearly 60%. Real estate prices fell for over a decade. Companies became technically insolvent.

Investment froze. Consumption weakened. Growth stalled.

This period became known as the “Lost Decades.” Wages stagnated. Inflation disappeared. Japan entered persistent deflation.

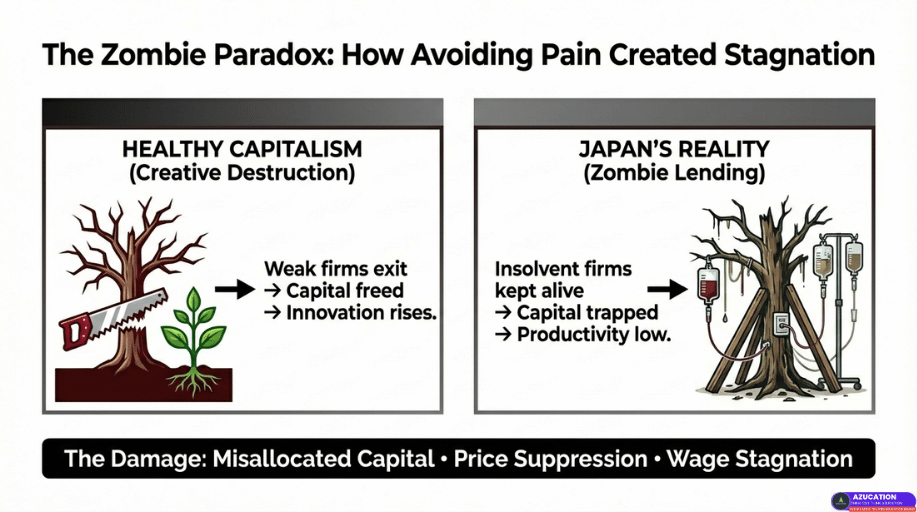

The Zombie Company Paradox

Instead of allowing creative destruction, banks refinanced struggling firms.

These “zombie companies” survived but did not grow. They misallocated capital, suppressed profits, blocked innovation, and slowed wage growth.

The cost of avoiding short-term pain became long-term stagnation.

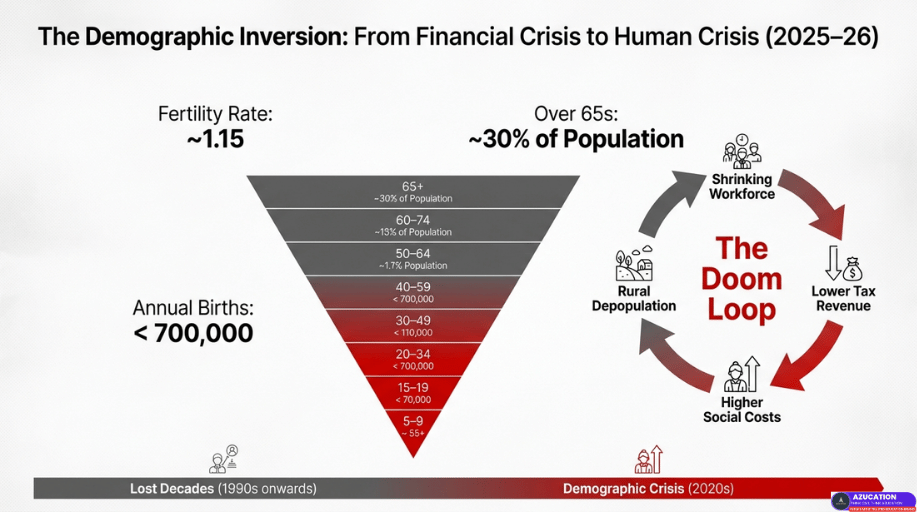

Demographic Collapse: The Structural Squeeze of the 2020s

Japan’s fertility rate has fallen to around 1.15. Nearly 30% of the population is above 65.

Labor shortages, school closures, shrinking towns, and business succession failures define modern Japan.

Japan is facing a demographic headwind that continuously pushes growth downward unless offset by massive productivity gains.

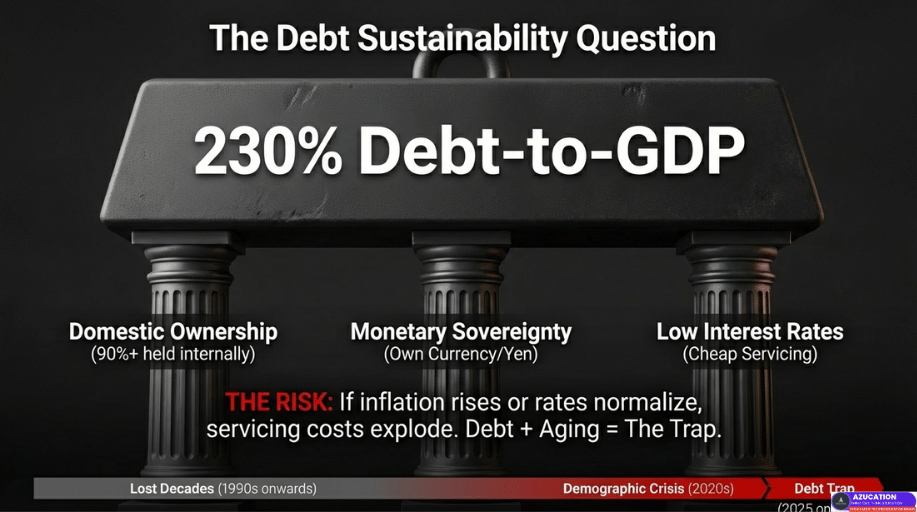

The Debt Question: Sustainability Under Strain

Japan’s public debt exceeds 230% of GDP.

While domestically financed, rising interest rates and aging costs create long-term sustainability concerns.

Debt alone is not a crisis. Debt combined with aging and slow growth is the risk.

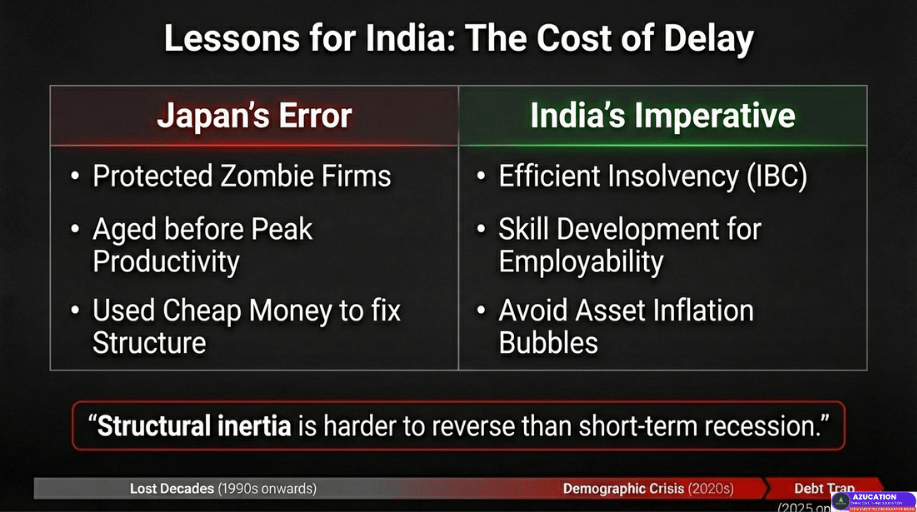

Lessons for India: What Must Be Avoided

India must learn:

• Capital allocation discipline is critical.

• Demographic dividend is temporary.

• Macroeconomic sequencing matters.

• Productivity must rise before demographic momentum slows.

Final Analytical Conclusion

Japan is not collapsing. It remains technologically advanced and globally integrated.

But it is experiencing structural compression created by past financial excess and demographic inversion.

The real danger in economics is rarely explosion. It is stagnation.

5 High-Impact IIM-Level Personal Interview Questions

The Plaza Accord was a trigger, not the structural cause. It accelerated existing vulnerabilities in Japan’s financial system.

The sharp appreciation of the yen reduced export competitiveness. To cushion the shock, the Bank of Japan aggressively lowered interest rates. The policy itself wasn’t flawed — the misallocation of credit was.

Instead of funding innovation or productivity upgrades, cheap liquidity fueled speculative investments in equities and real estate. Asset prices detached from fundamentals, creating one of the largest bubbles in modern history.

When tightening began in 1989, the bubble burst, exposing weak corporate balance sheets and excessive leverage.

Zombie companies are insolvent firms that survive due to continuous refinancing instead of bankruptcy.

After the asset bubble burst, banks rolled over bad loans to avoid recognizing losses. This avoided immediate panic but created systemic stagnation.

- Capital misallocation — funds remained locked in low-productivity firms.

- Industry margin suppression — weak firms competed aggressively to survive.

- Labor immobility — workers remained stuck in declining sectors.

Research shows that such “evergreening” of loans suppresses productivity growth economy-wide.

Japan’s debt structure differs significantly from crisis-hit nations like Greece.

- Majority of debt is domestically held.

- Debt is denominated in yen — Japan controls its currency.

- Low interest rates kept servicing costs manageable for decades.

However, risks remain. Aging increases fiscal burden. Rising rates could strain sustainability.

Full reversal is unlikely. Fertility has remained far below replacement for decades.

Policy responses include:

- Increasing female labor participation

- Extending retirement age

- Automation and robotics

- Selective immigration

- Raising productivity per worker

Japan cannot grow through population expansion anymore — it must grow through productivity.

Japan offers three structural lessons for India:

- Capital Discipline: Avoid protecting inefficient firms; ensure IBC efficiency.

- Demographic Urgency: Skill development must match population advantage.

- Policy Sequencing: Liquidity expansion must align with productivity reform.

Stagnation builds gradually when structural weaknesses are ignored.